Spreadsheets remain a legitimate part of the transfer pricing toolkit. They are flexible, widely understood, and well-suited to modelling, analysis, and review. The limitation is not what a spreadsheet can calculate. It is what a spreadsheet-based process cannot govern: data lineage across source systems, consistency across jurisdictions and entities, workflow and review controls, in-year monitoring, and the audit trail that connects policy to implementation to documentation. For multinational enterprises, that gap is no longer a process inconvenience. It is a control risk. This article examines where spreadsheet-based TP processes begin to strain, what a platform operating model changes, and how to assess when the transition makes sense.

The Real Question Is Not Whether Excel Works

Excel has earned its place in transfer pricing. It is flexible, familiar, and genuinely useful for modelling, review, and one-off analysis. Many sophisticated TP teams rely on it every day, and for good reason.

The issue is not whether Excel can support transfer pricing work. It can. The more important question is whether a spreadsheet-based process can provide the control, traceability, consistency, and audit readiness expected from a multinational enterprise operating across multiple jurisdictions, transaction types, data sources, and documentation cycles.

For many MNEs, the pressure point is no longer the calculation itself. It is the operating model around the calculation: how data is sourced, how assumptions are controlled, how local teams collaborate, how documentation is produced, how margins are monitored during the year, and how the organisation evidences that its transfer pricing policies have been applied consistently.

That is where spreadsheet-based processes begin to show their structural limitations. Not because the teams using them lack expertise, but because spreadsheets were not designed to function as enterprise control infrastructure for global transfer pricing.

A modern TP function needs more than a collection of well-maintained files. It needs a centralised data foundation, workflow governance, documentation logic, operational monitoring, and an audit trail that connects policy, data, analysis, approvals, and outputs. Excel may remain part of the toolkit. It should not be the system of record.

Where Spreadsheet-Based TP Processes Begin to Strain

Spreadsheet-based transfer pricing processes often work well in the early stages of a company's international growth. They provide flexibility, allow teams to build models quickly, and make it easy to adapt calculations as policies evolve.

The challenge emerges when those spreadsheets become the primary mechanism for managing global TP data, documentation, workflows, and controls. At enterprise scale, the limitations are structural.

Data lineage becomes difficult to evidence. TP-relevant data originates in ERP systems, consolidation tools, billing platforms, local finance files, and third-party data sources. Once extracted into spreadsheets, demonstrating how each figure moved from source system to calculation, documentation, and final filing becomes harder to sustain. The evidentiary challenge is not just producing the final analysis, but showing the source data, assumptions, review history, and the connection between policy and implementation.

Local versions of the truth multiply. Different jurisdictions maintain separate files, adjust local inputs, or work from different reporting dates. Even when each file is reasonable in isolation, consistency across the group becomes difficult to govern. When tax authorities request documentation, the reconciliation work that surfaces before submission is often the first visible sign of a structural limitation.

Change control depends on individual discipline. Spreadsheet models can be well-designed, but assumptions, formulas, and links can be changed without a structured approval process or complete review history. Model dependency and limited change control become risk factors as complexity grows and more people interact with the files.

Documentation becomes disconnected from the data layer. Local files, benchmarking support, intercompany transaction analyses, and financial schedules are often assembled manually from multiple sources. This creates avoidable reconciliation work and weakens the connection between policy, actual results, and documentation.

In-year monitoring is limited. A spreadsheet-based process typically supports year-end documentation better than ongoing management. For operational transfer pricing, teams need visibility into margins, segmented P&L, policy ranges, and potential adjustment needs throughout the year, not just when the documentation cycle opens.

These are not efficiency issues alone. They affect how confidently a multinational can demonstrate that its TP policies are implemented, monitored, documented, and governed at enterprise scale.

Why Transfer Pricing Templates Are Not a Control Framework

Many teams look for a transfer pricing Excel template as a more reliable path to compliant documentation. Templates are a useful starting point. They standardise output structure and ensure key analytical components are consistently present. They are not a TP control framework.

The specific limitations of a template-based approach at enterprise scale:

- No data integration. Templates require manual data entry. There is no live connection to ERP or financial systems, and no mechanism to ensure the data entering the template is current, reconciled, or consistent with underlying financials.

- Jurisdiction-specific logic depends on manual upkeep. A skilled user can build lookup tables for local materiality thresholds, safe harbours, or filing deadlines. The risk is governance: when Italy's materiality threshold changes, someone has to know it changed, update every affected file, and there's no system that confirms it was done consistently across the group.

- No workflow management or review trail. Templates do not track who has reviewed, approved, or signed off on a document. The approval process sits outside the document, which creates auditability limitations.

- Benchmarking is a weak system of record. Comparability searches are run in third-party databases and once the analysis is finalized, Excel doesn't reliably preserve the audit trail linking search criteria, rejected comparables and rationale, and the final accepted set.

- Limited scalability. A template that works for three entities becomes operationally difficult at thirty.

A template addresses the output format. It does not address the process, data governance, or control environment that should sit behind it.

What Changes When TP Moves to a Platform Operating Model

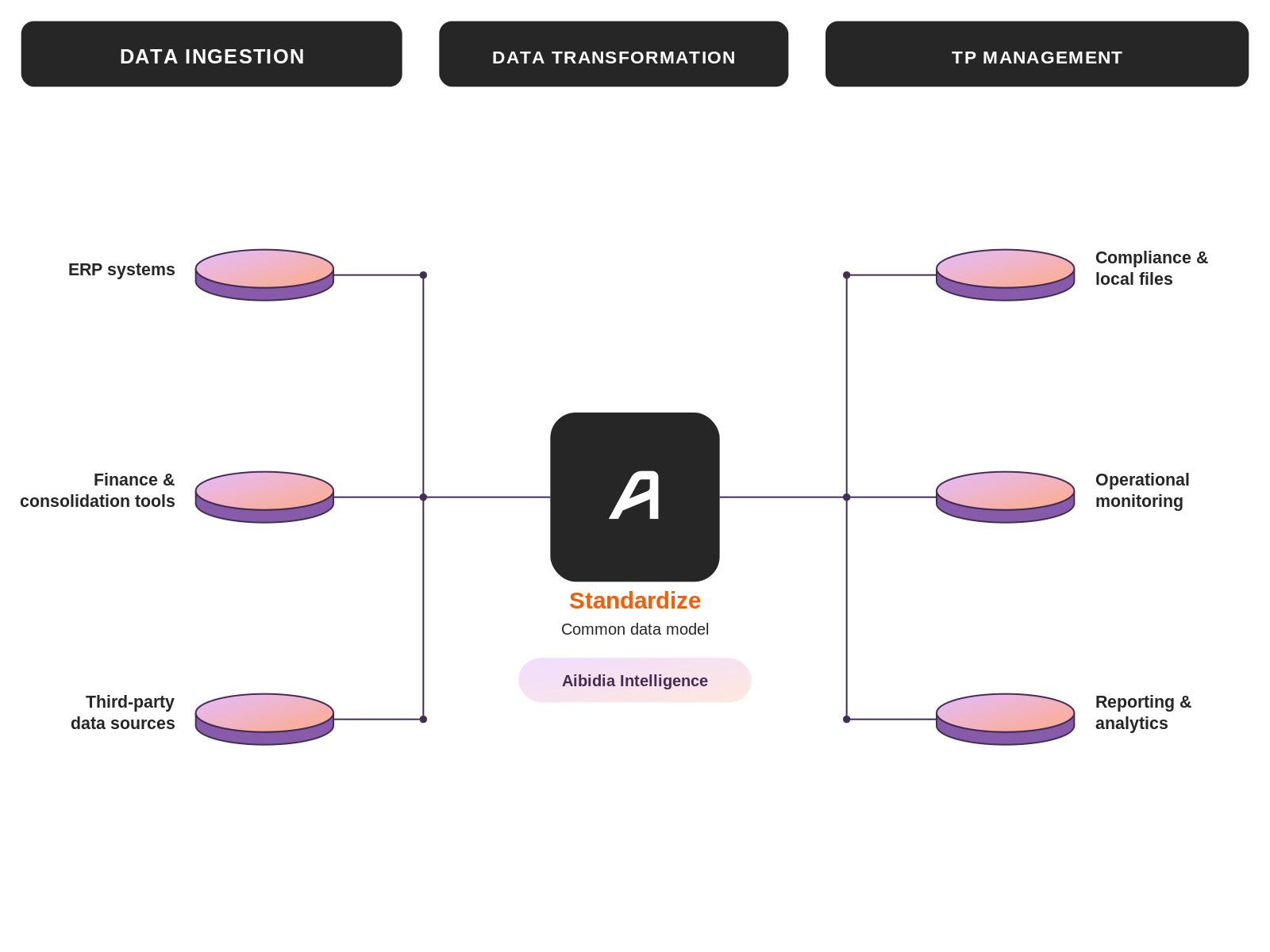

Moving beyond spreadsheets does not mean removing analytical flexibility from the TP function. It means moving the controlled process layer into an environment designed for enterprise-scale transfer pricing.

The core architectural difference is the data foundation. A transfer pricing platform connects directly to ERP systems and financial data sources. TP-relevant data is aggregated, standardised, and structured for compliance, analytics, operational monitoring, and reporting. Global tax teams, local finance teams, and external advisors work from a common basis rather than from independently-maintained local files.

Aibidia's platform is built around this principle. TP-relevant data from ERP systems and finance tools is centralised in one place, structured for compliance, operational monitoring, analytics, and reporting giving all teams a single source of truth for transfer pricing decisions.

From that centralised foundation, the TP function can manage core processes in a more connected way:

Automated local file production. Documentation is generated using standardised data and repeatable workflows, with jurisdiction-specific content structures applied automatically. The local file reflects the same underlying data as the group master, substantially reducing manual reconciliation.

Operational TP monitoring. Margins and intercompany results can be monitored during the year rather than reviewed only at year end. This gives teams the visibility they need to identify policy-to-actuals divergence and assess whether in-year adjustments are needed before the documentation cycle opens.

Segmented P&L analysis. Financial outcomes can be analysed by entity, business unit, product line, region, or other TP-relevant dimensions — giving both global tax and local finance a clearer view of how TP policy is tracking against actual performance.

Benchmarking support. Comparable analyses and supporting documentation can be managed in a structured, repeatable way, with the connection between search criteria, results, and documentation maintained within the platform.

Workflow and audit trail. Reviews, approvals, assumptions, and outputs are tracked as part of the process rather than reconstructed afterward. The evidentiary record is built in.

The important distinction is that a platform does not replace transfer pricing judgment. It strengthens the operating environment in which that judgment is applied, documented, reviewed, and defended.

What Are the Biggest Risks of Managing Transfer Pricing in Spreadsheets?

The risks of managing transfer pricing through spreadsheets are not primarily about calculation errors, though those are real. They are about the limitations of spreadsheets as a governance layer.

Limited auditability and evidentiary traceability. A growing number of authorities now factor governance and in-year management into risk assessment, and that trend is spreading. Even where it isn't a strict legal requirement, the ability to show ongoing management is increasingly what separates a defensible position from a vulnerable one when documentation connecting policy, data, calculation, and review is requested. Spreadsheet-based processes often require significant reconstruction work when that evidence is requested.

Inconsistency between policy, implementation, monitoring, and documentation. When each jurisdiction maintains its own files and there is no common data foundation, the risk that documentation does not accurately reflect what the business actually did increases with scale.

Version control limitations across entities, jurisdictions, and review cycles. There is no reliable mechanism in a spreadsheet environment to ensure every local team is working from current assumptions, approved models, or the latest policy positions.

Dependency on key individuals. Spreadsheet-based TP processes often concentrate knowledge in a small number of people who understand the model architecture. That is an operational risk that compounds over time.

Penalty exposure from documentation failures. Many jurisdictions impose documentation-specific penalties, assessed independently of the tax adjustment, and these are frequently traceable to process limitations: missing sign-off, stale data, or an inability to evidence how a position was reached.

These risks are manageable. The path is not necessarily a full overhaul. Many TP functions begin with one process area, often local file production or operational monitoring, and extend from there.

How Do You Move Transfer Pricing Out of Spreadsheets?

The transition from spreadsheets to a platform-based TP operating model does not require replacing everything at once.

Most TP functions approach this incrementally. The typical starting points are either compliance automation (replacing local file production first, then extending to benchmarking and documentation workflows) or operational transfer pricing, prioritising in-year monitoring and margin visibility where that risk is most immediate.

On implementation timelines: The timeline depends on scope, entity structure complexity, and the state of the underlying data. Compliance-focused implementations centered on local file automation typically reach initial output for review in six to twelve weeks, with full jurisdictional coverage across larger entity footprints typically spanning four to five months. Operational TP implementations are usually phased separately and take longer, particularly where underlying financial data needs to be cleaned or restructured.

Indicators that the business case has become clear:

- Reconciliation between local files and underlying financials requires significant manual effort each cycle

- In-year margin visibility is limited or dependent on manual reports

- The TP function has difficulty evidencing review and approval of documentation

- Growing local file volume is creating workload and coordination pressure

- Increasing scrutiny from tax authorities is exposing documentation quality gaps

- Complex intercompany transaction flows are difficult to track across disconnected files

- Pillar Two data requirements are adding further pressure to the entity-level data infrastructure

The trigger is rarely a single jurisdiction count. It is usually a combination of these complexity indicators arriving together.

What TP teams consistently report after making the transition is a reduction in documentation production time, elimination of the version control problem, and improved leadership visibility into compliance status across the group.

Yes. Excel remains useful for scenario analysis, ad hoc modelling, calculation review, and local analytical work. The question is not whether to use Excel, but whether spreadsheets should carry the burden of data governance, documentation production, workflow management, and audit evidence across a multinational TP function. Most modern TP functions use both: a platform for governed processes and structured data, and spreadsheets where analytical flexibility is the priority.

For small or early-stage international operations with limited intercompany transactions, Excel can support the basic requirements. As entity structure grows, transaction types diversify, and documentation expectations increase, the structural limitations become more significant. The core limitation is not calculation capability. It is that spreadsheets were not designed to operate as a multi-jurisdictional control environment with embedded workflow, data lineage, review history, and documentation logic.

The evidentiary challenge is that a spreadsheet documents the output, not the process that produced it. Tax authorities increasingly expect to see not just the final analysis, but the source data, the assumptions, who reviewed and approved the documentation, and how the results connect to the company's TP policy. That level of traceability is structurally difficult to provide from files maintained on shared drives with manual version control.

The trigger is rarely a single threshold. More often, it is a combination of complexity indicators: recurring reconciliation effort, inconsistent local file inputs, difficulty evidencing review and approval, limited visibility into in-year results, manual benchmarking workflows, growing entity and transaction volume, or increasing dependency on a small number of individuals who understand the spreadsheet architecture. When those factors arrive together, the business case for a governed platform environment typically becomes clear.